How Regulation Influences Innovation of Digital Financial Services: Evaluating the Different Approaches in Our Countries of Operation

By Abenaa Addai, MERL Consultant A2A Programme

Constant Learning and Knowledge Sharing

We have developed a set of learning questions within the A2A programme that help the programme partners, AccessHolding and Mastercard Foundation, to learn from own experience, draw on available knowledge, seek new explanations and connections, and thus generate new insights. The main purpose of our learning questions is to generate a body of knowledge that can be applied in practice within our group of banks, and also shared with the wider stakeholder network. Insights into our learning questions are documented in various formats such as videos, demos and written publications. In the following we summarize our learnings in an area, which becomes increasingly relevant with the advancing digital transformation of our banks in developing environments.

Learning Question: Which National Regulations and Settings Influence the Development of Digital Financial Products and Services?

The financial institutions in our network are increasingly offering innovative Digital Financial Services (DFS), in payments, lending and digital banking. DFS enabled by technological advancement and innovation have the potential to lower costs, increase speed, security and transparency, and allow for more tailored financial services that serve the poor at scale. The Covid-19 pandemic has amplified the benefits of expanding DFS in our banks because it significantly reduces the need for physical contact in retail banking and financial transactions. Accordingly, we have fast-tracked the development of several digital solutions to our clients, for example through remote customer on-boarding.

In this context we need to understand how regulation and regulatory settings influence the development not only of innovation at our banks and financial institutions but also the wider FinTech ecosystem in the countries we operate in. Each of our countries of operation is characterized by different legal and regulatory frameworks, financial and digital infrastructure, and a different ecosystem of fintech providers and users.

A Framework to Understand What Influences Digital Transformation

We commissioned a study to elaborate a framework which helps classifying different regulatory approaches of policy makers and regulators and outlining the main pillars or foundational elements that influence the development of digital financial products and services.

The framework we developed draws from important work done by the Pathways for Prosperity Commission (2019)1 and made use of fundamental compilation of the World Bank2. It looks at the driving factors of digital transformation in each country and assesses each country’s progress. Whilst it does not apply rigorously measurable indicators, it helps us understand the regulatory and foundational environment in which we launch our digital financial service innovations.

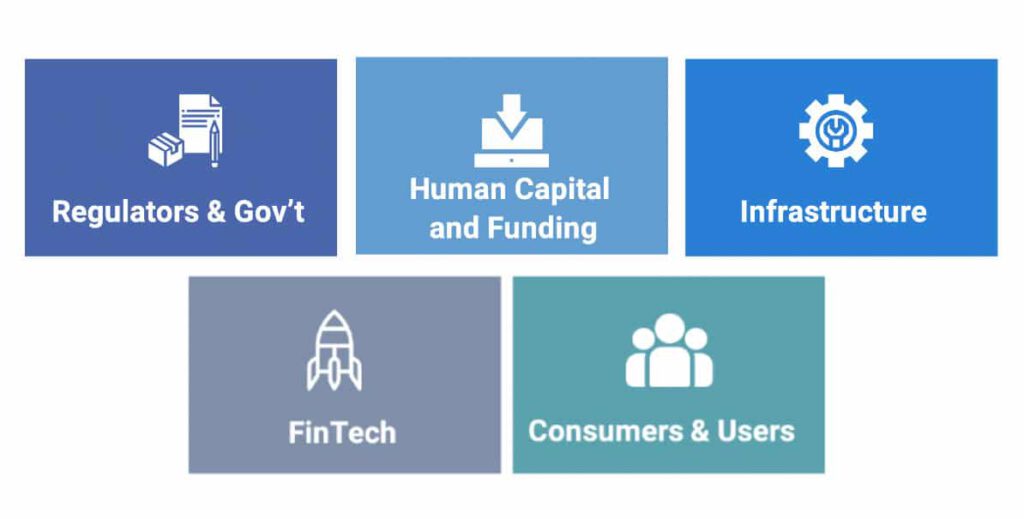

Five Pillars Enhance Digital Innovation

The interconnectedness and importance of the five pillars enhancing DFS innovation calls for an overarching digital transformation strategy.

- Regulators and Government engage to various degrees and through a variety of approaches in creating an enabling environment for the development of DFS while at the same time ensuring financial integrity, stability, competition and consumer protection. We based our analysis on the definition developed by the World Bank, which classifies regulatory response to digital innovation and the approaches to enhance digital transformation into “wait and see”, “test and learn”, “innovation facilitators” and “regulatory laws and reforms” for our countries of operation. We reviewed the advancement of our countries in creating an enabling fintech policy, legal, and regulatory environment through elements such as sandboxes and innovation hubs.

- Human Capital and Funding drives innovation in form of a digital savvy workforce and access to capital for FinTechs over the lifecycle, from the early stages of operation through to expansion. We looked at the existence of workforce with digital skills and whether the environment to attract and retain talent was given. The access to finance and funding can be granted through financing and incentive programs for early-stage entrepreneurs and by growing angel-investor networks.

- An enabling underlying digital infrastructure is at the core of a digital economy. Digital infrastructure includes the physical and software infrastructure necessary for connectivity such as high-speed internet and internet exchange points, Internet of Things (such as mobile devices, computers and sensors), and data repositories (such as data centers and clouds). It also englobes well-functioning payment systems and switches enabling interoperability as well as end user devices. Digital platforms facilitate communications, transactions, and service delivery digital channels. Digital public sector platforms as a wider part of e-government systems are an important part in developing digital infrastructure.

- The developing grounds for FinTechs must be given to have a thriving offer of automated and improved financial services embracing new financing instruments, new financial services as well as new financial intermediaries. This may include support organizations that provide incubators and innovation hubs, accelerator programs and generally business support for the creation of a digital entrepreneurship.

- The demand for innovative DFS is driven by the needs of Consumers and Users and FinTech can reach customers and business segments that are not adequately serviced by traditional financial service providers. Generating demand in turn requires creating access to adequate technology (mobile device penetration, internet usage) as well developing digital skills to use information technologies effectively. A well-developed e-Gov strategy can strongly support demand for new DFS.

Spotlight on our countries

In our countries of operation, the regulatory approaches as well as the development of the other four pillars is very heterogeneous. Whilst some countries (like Rwanda) see digitalization as a way to accelerate growth and have adopted a national strategy of transformation, we found that others (like Liberia) lack clarity and consistency of regulatory and legal frameworks. We found no common approach to enhance DFS innovation applied across our countries and that an agile adaptation to changing environment was predominant.

We also looked at the regulatory impact of the COVID 19 crisis and found that as a first response to the crisis, most governments focused their – mostly temporary – regulatory adjustments on “quick wins” that had a high potential to mitigate part of the impact of the pandemic on the national economy.

A spotlight on the status of digital transformation in three countries of our countries of operation can be found here.

The full report compiling the findings on the regulatory and policy approach applied to enhance the offering of digital financial services, can be found here.

Access2Access

The Access2Access (A2A) programme was set-up in summer 2016 with a total value of USD 33 million. In September 2016, AccessHolding entered into a Partnership Agreement with Mastercard Foundation to support the A2A Programme with USD 15.5 million over a period of five years. The overall objective of the A2A programme is to strengthen the capacities of the AccessHolding Network Financial Institutions (NFI) with the aim to increase outreach and improve access to financial services that meet client needs more efficiently and profitably. The partnership with Mastercard Foundation has two components: (i) Capacity Building and (ii) Digitalisation. The Capacity Building component strengthens human resources of the NFIs by supporting AccessCampus (network-wide education of middle managers), AccessFoundation (training of trainers and local advanced learning for all staff) as well as the development and implementation of an e-learning platform (AccessMind). The intensive and diversified Capacity Building initiatives qualify staff to manage complex changes related to the introduction of digital products and services, and to put the customer in the centre of all developments. The Digitalisation component broadens the range of channels, products and services that customers can access, based on a client-centric business model. At the same time the new developments improve the institutions’ internal efficiency, and are built on a solid, scalable, flexible and secure IT architecture.

The reports can be downloaded below.